Disclosures

Website Privacy

When you visit transwestcu.com, TransWest Credit Union may collect private information that you choose to give by completing forms or feedback. Portions of our website may use Google Analytics, which is a web analytics service provided by Google, Inc. This service uses “cookies”. “Cookies” are small text files placed on your computer’s hard drive, to help us analyze how individuals use our site. “Cookies” do not collect any personal identification information. TransWest Credit Union will use this data as we strive to provide a better experience when you return to our site. You may opt out of the use of Google Analytic cookies by selecting the appropriate setting in your browser. You may also opt out of Google Analytics Advertising features through Google Ad Settings . Learn more about Google’s Data and Privacy Security .

By clicking the hyperlinks you will be leaving the TransWest Credit Union site. By accessing the noted links you will be leaving TransWest Credit Union’s website and entering a website hosted by another party. TransWest Credit Union has not approved this as a reliable partner site. Please be advised that you will no longer be subject to, or under the protection of, the privacy and security policies of TransWest Credit Union’s website. We encourage you to read and evaluate the privacy and security policies of the site you are entering, which may be different than those of TransWest Credit Union.

Privacy Policy

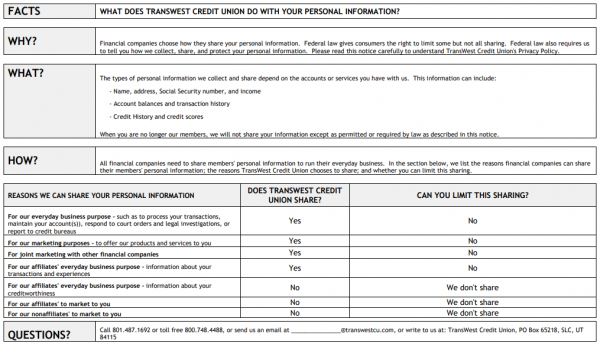

TransWest Credit Union protects the privacy of its members (and other consumers) in accordance with applicable federal and state law. The Credit Union collects information about consumers from applications or other forms from transactions conducted with the Credit Union, from consumer reporting agencies, and from government agencies such as the Department of Motor Vehicles.

We may disclose all of the information we collect, as described above, to companies that perform marketing services on our behalf or to other financial institutions, such as insurance companies, with whom we have joint marketing agreements.

“Nonpublic personal information” about you is restricted to those employees who need to know that information to provide products or services to you. We maintain physical, electronic and procedural safeguards that comply with federal regulations to guard your nonpublic personal information.

Request deletion of mobile/online banking user profile

Google and Apple are requiring that all mobile applications provide a method for users to delete their mobile/online banking user profiles. This requirement is the latest of many recent compliance updates from Google and Apple related to user privacy and data safety.

If you would like to request removal of your mobile/online banking user profile and related data, simply send an email request to [email protected]

Please type “Remove mobile/online banking profile” in the subject line of your email and provide us with a good phone number to reach you at. One of our representatives will be in touch with you to confirm the request is valid and initiate the process.

Upon execution of this request, any activity you previously set up within online banking or our mobile app will be disabled and/or deleted. This includes real-time account alerts, Bill Pay payments and payee info, External Transfers, scheduled or recurring transfers, as well as any history for any of these services. Your accounts will remain active, and your accounts transaction history will remain in our main system history as long as your accounts are open.

CardCierge Privacy Policy

TransWest Credit Union values and strives to protect the privacy of its members. The CardCierge app collects information through the creation of your CardCierge account, transactions conducted within that account, from consumer reporting agencies, including credit bureaus, feedback from users, and through continual use of the app.

We may disclose the information we collect to those companies who work closely with TransWest Credit Union and the CardCierge app to provide its users with a quality service optimized for performance.

It is TransWest Credit Unions goal to maintain safeguards that comply with federal regulations to guard the nonpublic personal information gathered using the CardCierge app.

To learn more about the CardCierge Privacy Policy, click here .

Fee Schedule

The Credit Union provides most services at no charge. However, there are some services that do require a fee. Please view our Fee Schedule below to learn more about these services.

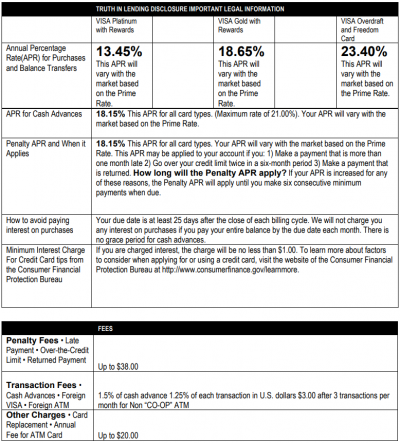

VISA Rates and Disclosure

VISA Gold and Platinum Credit Cards, VISA Debit Card, and TransWest Credit Union ATM Card

How We Will Calculate Your Balance: We use a method called “average daily balance (including new purchases).”

Billing Rights: Information on your rights to dispute transactions and how to exercise those rights is provided in your account agreement.

Periodic Rates:

The VISA Platinum with Rewards APR is 13.45% which is a daily periodic rate of 0.036849%.

The VISA Gold with Rewards APR is 18.65% which is a daily periodic rate of 0.051096%.

The Cash Advance APR is 18.15% which is a daily periodic rate of .049726%

The Penalty APR is 18.15% which is a daily periodic rate of .049726%

TRUTH-IN-LENDING DISCLOSURE-IMPORTANT LEGAL INFORMATION

Approved Credit Counseling Agencies

For those individuals who feel they need credit counseling, the following Credit Counseling Agencies are approved by TransWest Credit Union:

Consumer Credit Counseling Service of Utah

720 S. River Road Bldg. C-235

St. George, UT 84770

800-451-4505

English and Spanish Globous Financial Relief

1775 W. 1500 South

Salt Lake City, UT 84104

801-977-0555

Granite Lake Educational Resources

641 West North Temple Suite 60

Salt Lake City, UT 84116

866-366-0599

English and Spanish

For additional counseling services that are also approved, please search for an agency near you by visiting U.S. Department of Justice list of approved Credit Counseling Agencies.

If you need additional information, please speak with a TransWest Credit Union Customer Service Rep. by calling toll free 1-800-748-4488.

1. Responsibility.

If we issue you a card, you agree to repay all debts and the FINANCE CHARGE arising from the use of the card and the card account. You are also responsible for charges made by anyone else to whom you give the card, but we will close the account for new transactions if you so request and return all cards. Your obligation to pay the account balance continues even though an agreement, divorce decree or other court judgment to which we are not a party may direct you or one of the other persons responsible to pay the account. Any person using the card is jointly responsible with you for charges he or she makes.

2. Lost Card Notification.

If you notice the loss or theft of your credit card or a possible unauthorized use of your card, you should write to us immediately at the address listed on your bill or call us at 1-801-487-1692 or 1-800-748-4488. After regular business hours, call 1-800-543-5073. Outside of the U.S.A., call 1-727-570-4881. You will not be liable for any unauthorized use that occurs after you notify us. You may, however, be liable for unauthorized use that occurs before your notice to us. In any case, your liability will not exceed $50.

3. Credit Line.

If we approve your application, we will establish a self-replenishing Line of Credit for you and notify you of its amount when we issue the card. You agree not to let the account balance exceed this approved Credit Line. Each payment you make on the account will restore your Credit Line by the amount of the payment which is applied to principal. You may request an increase in your Credit Line only by completing a new VISA application. By giving you written notice, we may reduce your Credit Line at any time, or with good cause, revoke your card and terminate this Agreement. Good cause includes your failure to comply with this Agreement or adverse re-evaluation of your credit worthiness. You may also terminate this Agreement at any time, but termination by either of us does not affect your obligation to pay the account balance. The cards remain our property and you must recover and surrender to us all cards upon our request and upon termination of this Agreement.

4. Credit Information.

You authorize us to investigate your credit standing when opening, renewing or reviewing your account. You authorize us to disclose information regarding your account to credit bureaus and other creditors who inquire of us about your credit standing. We may also disclose information to third parties about your account or the transfers you make where it is necessary for completing transfers; or in order to comply with government agency or court order; or if you give us your written permission. We will not disclose account information to credit bureaus on persons under 18 years of age.

5. Monthly Payment.

We will mail you a statement or send you an eStatement every month showing Previous Balances, of purchases and cash advances, current transactions on your account, remaining credit available under your Credit Line, New Balances of purchases and cash advances, Total New Balance, FINANCE CHARGE due to date, and the Minimum Payment required. Every month you must pay at least the Minimum Payment within 25 days of your statement closing date. You may reduce the FINANCE CHARGE by paying more frequently, paying more than the Minimum Payment, or by paying the Total New Balance in full. Your

Minimum Payment will be 3% of your Total New Balance, or $20.00 – whichever is greater or the Total New Balance if less than $20.00, plus any portion of the Minimum Payment(s) shown on prior statement(s) which remains unpaid. In addition, at any time your Total New Balance exceeds your Credit Line, you must immediately pay the excess upon our demand. We will apply your payments first to previously billed and unpaid FINANCE CHARGE on purchase; then to previously billed and unpaid FINANCE CHARGE on cash advances; previously billed purchases; cash advances; and then to new purchases, whether or not billed on the monthly statement. However, any payment equal to, or greater than, the Previous Balance of Purchases will be applied first to that balance and any FINANCE CHARGE thereon to avoid continuing accrual of FINANCE CHARGE on that amount.

6. Finance Charges.

25-DAY GRACE PERIOD. You can avoid FINANCE CHARGE on purchases by paying the full amount of the New Balance of Purchases each month within 25 days of your statement closing date. Otherwise, the New Balance of Purchases, and subsequent purchases from date they are posted to your account, will be subject to a FINANCE CHARGE.

CASH ADVANCES. There is a 1.5% cash advance fee and there is no grace period on a cash advances. Interest will be charged from the day the advance is posted to your account.

FINANCE CHARGE. The ANNUAL PERCENTAGE RATE may vary. The VISA PLATINUM with Reward Points APR is 13.45% which is a daily periodic rate of .036849%. This rate is determined by adding 4.95% to the U.S. Prime Rate. The VISA GOLD with Reward Points, APR is 18.65% which is a daily periodic rate of .051096%. This rate is determined by adding 10.15% to the U.S. Prime Rate. The CASH ADVANCE APR is 18.15% which is a daily periodic rate of .049726%. The PENALTY APR is 18.15% which is a daily periodic rate of .049726%. The OVERDRAFT APR is 23.40% which is a daily periodic rate of .064109%.The maximum penalty rate is 21%. The ANNUAL PERCENTAGE RATE will be adjusted quarterly based on the “U.S. Prime Rate” as listed in the “Money Section” of the Wall Street Journal on the third Tuesday of March, June, September and December. The interest rate on existing balances will be adjusted on the last day of the quarter. The maximum interest rate will never exceed the rate permitted under Utah law. There is no maximum change in the interest rate in any quarter. A FINANCE CHARGE on the daily balance of purchases will be assessed from the date the purchase transaction is posted to your account unless the “New Balance” shown on your previous statement was paid in full on or before the due date shown. If you elect to pay your account in installments, or you do not pay in full by the date shown on your monthly statement, you shall pay a periodic FINANCE CHARGE on your unpaid purchases and advances. We figure the interest charge on your account by applying the periodic rate to the “average daily balance” of your account. To get the “average daily balance” we take the beginning balance of your account each day, add any new purchases, advances or fees, and subtract any unpaid interest or other finance charges and any payments or credits. This gives us the daily balance. Then, we add up all the daily balances for the billing cycle and divide the total by the number of days in the billing cycle. This gives us the “average daily balance.”

7. Default. (Not Applicable to Minors)

You will be in default if you fail to make a Minimum Payment within 25 days after your monthly statement closing date. You will also be in default if your ability to repay us is materially reduced by a change in your employment, an increase in your obligations, bankruptcy or insolvency proceedings involving you, your death or your failure to abide by this Agreement, or if the value of our security interest materially declines. If you default, the entire balance of this account shall become due and payable at the option of the Credit Union. Each party hereto further agrees that if payment of the account shall not be made as herein provided, you shall pay the costs of collection, including a reasonable attorney’s fee. The Credit Union can delay enforcing any of its rights under this Agreement without losing them. If you are in default (more than 30 days past due) you will lose any accrued reward points attached to your card or other card rewards which you may have accumulated.

8. Using the Card.

To make a purchase or cash advance, there are two alternative procedures to be followed. One is for you to present the card to a participating VISA plan merchant, to us or another financial institution. The other is to complete the transaction by using your Personal Identification Number (PIN) in conjunction with the card in an Automated Teller Machine or other type of electronic terminal that provides access to the VISA system. The monthly statement will identify the merchant, electronic terminal or financial institution at which transactions were made, but sales, cash advance, credit or other slips cannot be returned with the statement. The Credit Union may make a reasonable charge for photocopies of slips you may request. You may not use your VISA Card for any illegal transactions. Effective March 1, 2001, VISA and Trans West Credit Union will automatically decline identifiable online (Internet) gambling transactions on VISA Platinum, Gold, and VISA.

9. Returns and Adjustments.

Merchants and others who honor the Card may give credit for returns or adjustments, and they will do so by sending us a credit slip which we will post to your account. If your credits and payments exceed what you owe us, we will hold and apply this credit balance against future purchases and cash advances or if it is $1.00 or more, refund it on your written request or automatically after six months.

10. Foreign Transactions.

Purchases and cash advances made in foreign countries, either in U.S. dollars or foreign currencies will be billed in U.S. dollars. The conversion rate to dollars will be made in accordance with the operating regulations for international transactions established by VISA International, Inc. There may be a fee charged for VISA purchases made in foreign countries due to currency exchange rate differences.

11. Security Interest.

To secure your account, (unless you are a minor) you grant us a purchase money security interest under the Uniform Commercial Code in any goods you purchase through the account. If you default, we will have the right to recover any of these goods which have not been paid for through our application of your payments in the manner described in paragraph 6. If you give, or have given us a specific pledge of your credit union shares by signing a pledge of shares agreement, your account will also be secured by your pledged shares and by the property described in those other security agreements. As a convenience and if funds are available, you can give us permission to transfer funds from your checking account or from any of your savings accounts to make your payment.

12. Effect of Agreement.

This Agreement is the contract which applies to all transactions on your account even though the sales, cash advance, credit or other slips you sign or receive may contain different terms. We may amend this Agreement from time to time by sending you advance written notice required by law. Your use of the card thereafter will indicate your agreement to the amendments. To the extent the law permits, as we indicate in our notice, amendments will apply to your existing account balance as well as to future transactions.

13. Change of Terms.

The Credit Union reserves the right to alter the terms of this agreement and will give notice of any change in terms as required by applicable law. These changes may include, but are not limited to, any change in the FINANCE CHARGE.

14. Final Expression.

This Agreement is the final expression of the terms and conditions of this VISA line of credit between you and the Credit Union; this written Agreement may not be contradicted by evidence of any alleged oral agreement.

15. Other Charges.

The following charges may be added to your account at the end of each statement date, as applicable: any direct fees associated with special inquiries which you initiate (such as photocopies, original copies, etc.) at par.

16. Late Fee.

A late fee of $25.00 shall be charged whenever any payment is not paid within 15 days of its scheduled due date. The maximum late fee is $25 for the first late payment and $35 for each consecutive late payment after the first. If you are more than 30 days past due, you will lose any accrued ScoreCard points or other card rewards which you may have accumulated.

Your Billing Rights

KEEP THIS NOTICE FOR FUTURE USE

This notice contains important information about your rights and our responsibilities under the Fair Credit Billing Act.

Notify Us In Case of Errors or Questions about Your Bill

If you believe your bill is wrong, or if you need more information about a transaction on your bill, write to us on a separate sheet at the address listed on your bill. Write to us as soon as possible. We must hear from you no later than 60 days after we have sent you the first bill on which the error or problem appeared. You can telephone us, but doing so will not preserve your rights. In your letter, give us the following information:

* Your name and account number.

* The date and dollar amount of the suspected error.

* Describe the error and what has been done to correct the error with the merchants. Explain, if you can, why you believe there is an error. If you need more information, describe the item you are not sure about.

If you have authorized us to pay your credit card bill automatically from your savings or checking account, you may stop the payment on any amount you question. To stop payment, your letter must reach us three business days before the automatic payment is scheduled to occur.

Your Rights and Our Responsibilities After We Receive Your Written Notice

We must acknowledge your letter within 30 days, unless we have already corrected the error. Within 90 days, we must either correct the error or explain why we believe the bill was correct. After we receive your letter, we cannot try to collect any amount you question, or report you as delinquent. We can continue to bill you for the amount you question, including finance charges, and we can apply any unpaid amount against your credit limit. You do not have to pay any questioned amount while we are investigating, but you are still obligated to pay the parts of your bill that are not in question. If we find that we made a mistake on your bill, you will not have to pay any finance charges related to any questioned amount. If we didn’t make a mistake, you may have to pay finance charges, and any missed payments on the questioned amount. In either case, we will send you a statement of the amount you owe and the date that it is due. If you fail to pay the amount you owe, the Credit Union may report you as delinquent. However, if our explanation does not satisfy you and you write to us within ten days telling us why you refuse to pay, we must tell anyone we report you to that you have a question about your bill. We must notify you of anyone to whom you were reported. When the matter is settled between us, we must tell anyone to whom you were reported that the matter has been resolved. If we don’t follow these regulations, we cannot collect the first $50 of the questioned amount, even if your bill was correct.

Special Rule for Credit Card Purchases

If you have a problem with the quality of property or services that you’ve purchased with a credit card, and you have tried in good faith to correct the problem with the merchant, you may have the right not to pay the remaining amount due on the property or services. There are two limitations on this right.

(a) You must have made the purchase in your home state or, if not within your home state, within 100 miles of your current mailing address; and

(b) The purchase price must have been more than $50. These limitations do not apply if we own or operate the merchant, or if we mailed you the advertisement for the property or services.

Reporting a Lost or Stolen VISA Card

If you believe your VISA Card has been lost or stolen or that someone has transferred or may transfer money from your account without your permission, call;

Lost Card: Call 801-487-1692 or 1-800-748-4488 (Long Distance)

After Regular Hours: Call 1-800-543-5073 (VISA Only)

Outside the U.S.A.: Call 1-727-570-4881.

Contact a TWCU Branch

If you have a VISA Platinum and/or Gold Card, get emergency assistance at: 1-800-VISA-911. Outside the U.S.A. call collect 1-410-581-9994.